Three of the world’s most talked-about companies are heading for the US stock market. SpaceX, OpenAI and Anthropic, behind rocket launches, ChatGPT, and Claude respectively, have spent years as privately held businesses.

Together, their listings could raise more money in 2026 than the US IPO market has ever seen in a single year.

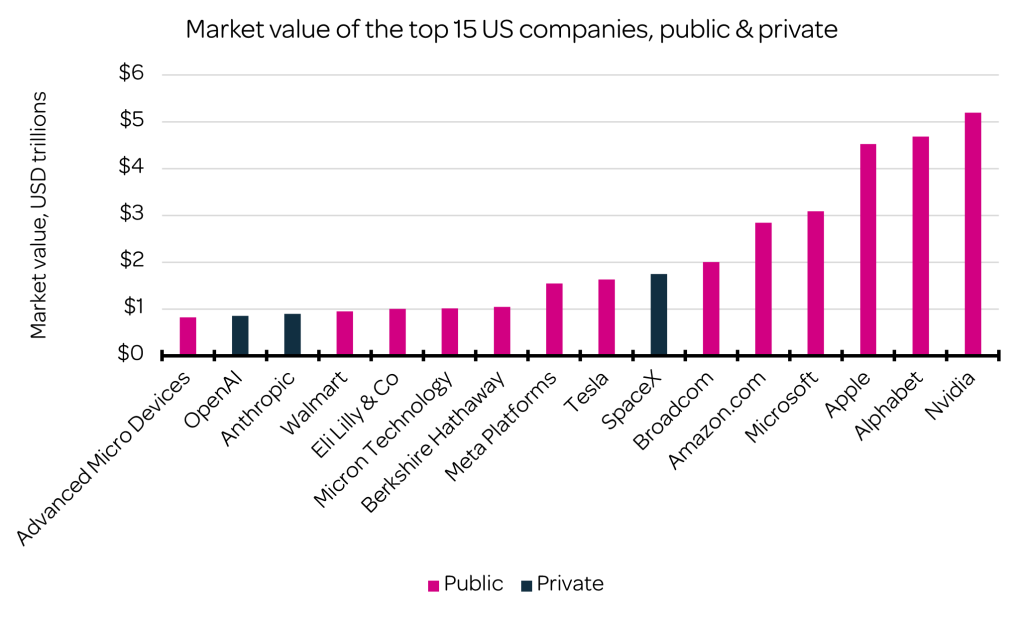

The names behind the numbers

A brief introduction to each may be useful given the private nature of these companies.

OpenAI makes ChatGPT, the chatbot launched in late 2022 that became one of the fastest-adopted consumer products in history. It is on track for around $30bn in annualised revenue but has told investors it expects to spend roughly $600bn before turning a profit at the end of the decade.

Anthropic owns Claude, a rival chatbot that has grown quickly in the corporate market and now generates around $40bn of annual recurring revenue.

SpaceX, founded by Elon Musk in 2002, designs the reusable rockets that have turned satellite launches from costly milestones into routine operations, and it owns Starlink, the satellite internet business that sits inside it.

Last year, SpaceX merged with X (formerly known as Twitter), bringing Musk’s social media and AI venture, xAI which owns the Grok chatbot, under one corporate structure

Private valuations are taken from latest publicly disclosed values. Public valuations retaken from last market close. Source: Bloomberg, EQ Investors. Data as at 27/05/2026.

A rare window – and why it matters

The scale of these listings is the part worth pausing on.

At the valuations bankers are targeting, SpaceX would come to market at $1.75tn and OpenAI close to $1tn, making them larger on day one than any of the famous IPOs that came before. Visa, Meta, Alibaba and General Motors were the four largest US flotations of the past 30 years. Each raised between $16bn and $25bn. SpaceX alone is aiming for $75bn.

Part of what makes this moment unusual is how rare blockbuster IPOs have become. Businesses have stayed private for longer, fewer have come to market, and those already listed have bought back shares or merged with one another. The number of US-listed companies has more than halved since 1995 – a trend that has also been experienced in Europe and the UK.

The result has been a shrinking pool of listed companies. A wave of mega-IPOs reverses that pattern and is likely to result in several new high-profile companies coming to market.

Hype and reality

For most investors, the practical implications are narrower than the headlines suggest.

Those looking to take part in IPOs, particularly those as high profile as these, rarely receive a full allocation at the IPO price. The more important point is how investors’ exposure to themes such as AI or space is set to increase without any deliberate investment decision being made.

Together, SpaceX, OpenAI and Anthropic could well become large constituents of mainstream equity indices like the S&P 500 or the MSCI AC World meaning passive investment strategies that replicate index holdings will need to buy meaningful positions.

Much of this will depend on something called the “free float” which measures how much of a company’s equity is considered not tradable. This could either be because it is owned by company insiders (Elon Musk owns around 40% of SpaceX) or because it is held by long-term strategic shareholders.

This can have a material impact on inclusion within indices. SpaceX is coming to market with less than 10% of its equity considered freely floating. This means that despite the eyewatering headline valuation, SpaceX may make up less than 0.20% of indices like the S&P 500 – significantly lower than other public companies with similar headline valuations.

For the more cautious investors, big IPO waves tend to arrive when markets are already running warm and when investor sentiment is high.

Public investors are often less patient than the private backers who got there first. Grand visions can survive contact with public markets, but they are also stress-tested by them. Deliveroo is a good example of this in the UK equity market with its shares falling materially after its initial offering.

Our positioning

Inclusion of these companies in EQ portfolios will vary. The portfolios we manage employ different approaches and have different aims. Some exclusively use active managers while others may be exclusive passive, or a hybrid mix of the two. The inclusion of companies such as SpaceX is difficult to predict at this stage.

Many active managers may baulk at the IPO valuations, while passive investment vehicles will ultimately buy shares in the proportion of the indices that they track. This is something we will be watching as time goes on.

Our preference is always to maintain diversified exposure to the long-run opportunity in themes such as artificial intelligence. The themes driving these listings are present in portfolios already, at least in part, just not in concentrated form.

Any questions?

If you would like more information about EQ’s investment views and services, please get in touch.

Please remember, this content is provided for information purposes only. Investment involves risk. Past performance is not a guarantee or indication of future results. Investment return and the principal value of an investment may go up or down and may result in the loss of the amount originally invested. All investors should seek professional advice prior to any investment decision, to determine the risks associated with the investment and its suitability.