State of affairs

Following the recent invasion of Ukraine by Russia, European leaders have been reminded of the region’s high dependency to fossil fuels extracted in Russia. Addressing Europe’s energy independence is going to be a mammoth task, but increasingly necessary for politicians wanting to limit reliance on Russia. More than 40% of Europe’s natural gas imports come from Russia so achieving energy security will require a dramatic shift in policy. Fortunately, policymakers have several options.

We could see some of the dirtier fossil fuels such as coal used in greater quantities. However, a good proportion of Europe’s coal imports also come from Russia, and dirtier fuels would be counterproductive to existing climate change goals. There has been some discussion in the UK around whether fracking rules should be changed. But new natural gas-fired plants take two to three years to bring online.

There has also been some debate around how nuclear power can play a role in the energy mix. But new nuclear capacity is also likely to come online too late. Reactors regularly take more than 10 years to complete – construction of the UK’s Hinkley Point C began in 2018 and is not expected to come online before 2026, 14 years after it was first approved.

Fortunately, there is an attractive solution that is consistent with climate change goals and has shorter lead times: renewables. Unlike the years-long timescales for nuclear and gas, a solar installation will take approximately six months to bring online (depending on the size and scale of the project), while small-scale wind farms can be built in as little as two months.

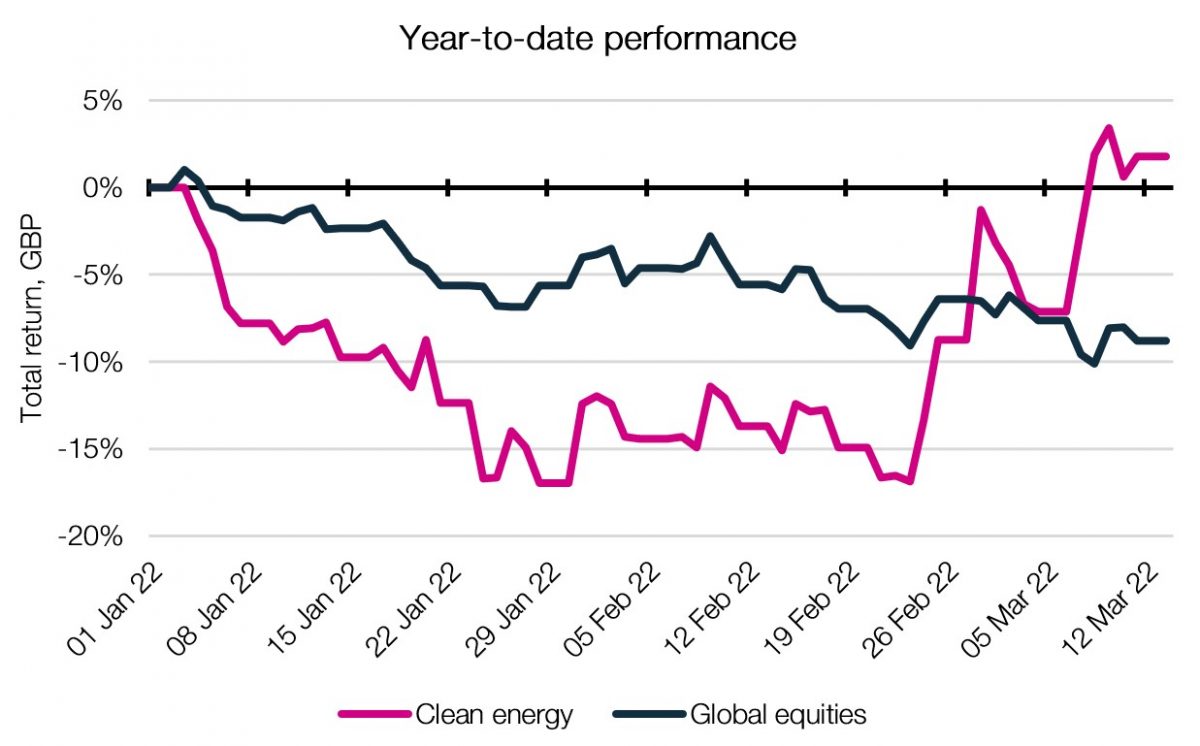

Market valuation

Since the start of the year, many renewable energy companies had seen their share prices dropping by 20% or more until the conflict in Ukraine started. This was due to rising concerns for inflation, where faster growing companies had seen an almost indiscriminate selling pressure regardless of whether underlying businesses were performing well or not versus expectations.

Consequently, clean energy stocks have been trading at valuations at or below levels prior to the announcement of the US infrastructure plan which significantly boosted the growth expectations for the sector. It is therefore no surprise to see the renewable energy sector bounding back sharply since the invasion of Ukraine as governments highlighted their ambition to become energy independent.

Source: Morningstar, EQ Investors

Despite this recent bounce back, we believe that the renewable energy sector is still trading at attractive valuations as the long-term prospects of renewable energy companies remain underestimated by the market. Though there may be some shorter-term re-alignments to increase energy security, many governments around the world are committed to the long-term goals of achieving net zero emissions by 2050.

To do this, new solar farms will require more specialist glass equipment and wind farms will need more blades and turbines. So, the adoption of renewable energies globally (and particularly in Europe) is likely to accelerate in the coming years as they provide a partial but necessary solution to reduce dependency on Russian gas. Until now, there have been barriers to rolling out renewables at a large scale such as an inherent volatility in solar or wind generation. But developments in energy storage is providing a solution to this intermittency. Finally, the rise in fossil fuel prices is making renewable business models even more attractive from a financial perspective.

Portfolio exposure

Within our portfolios, we gain exposure to this theme in several ways, most notably through underlying equities such as Ørsted and Vestas Wind Systems. Both companies are listed in Denmark, and feature across most of our portfolios at EQ Investors.

Ørsted, formerly known as DONG Energy (or Danish Oil & Natural Gas), has become a world leader in offshore wind power following an accelerated programme to retire its fossil fuel assets and develop offshore wind capacity. The company has developed approximately 30% of the global offshore wind capacity and now produces over 90% of its energy from renewable sources. As European nations look to secure their energy independence, it’s likely that companies such as Ørsted will be front and centre of capacity expansion given their expertise in the field.

Vestas Wind Systems is a leading manufacturer and servicer of wind turbines, with production facilities around the globe. With its wind farm developer partners, Vestas’ turbines are responsible for more than 150 GW of wind power capacity in more than 70 countries. While power companies such as Ørsted are likely to be directly involved in co-ordinating wind farm development, Vestas Wind Systems is the supplier of choice for many other power companies meaning it is a broader way of gaining exposure to increased demand from wind developers across the world.

The time for renewables is now

The need to secure homegrown energy supplies and fight climate change, means renewables should be the key pillar of the new government energy strategy. This will help free the UK from dependence on imported oil & gas and spare households and businesses from the effects of wild fluctuations on global energy markets.

With smarter grid plus storage, we also believe that it will be virtually impossible to compete against renewables economically by the end of the decade.